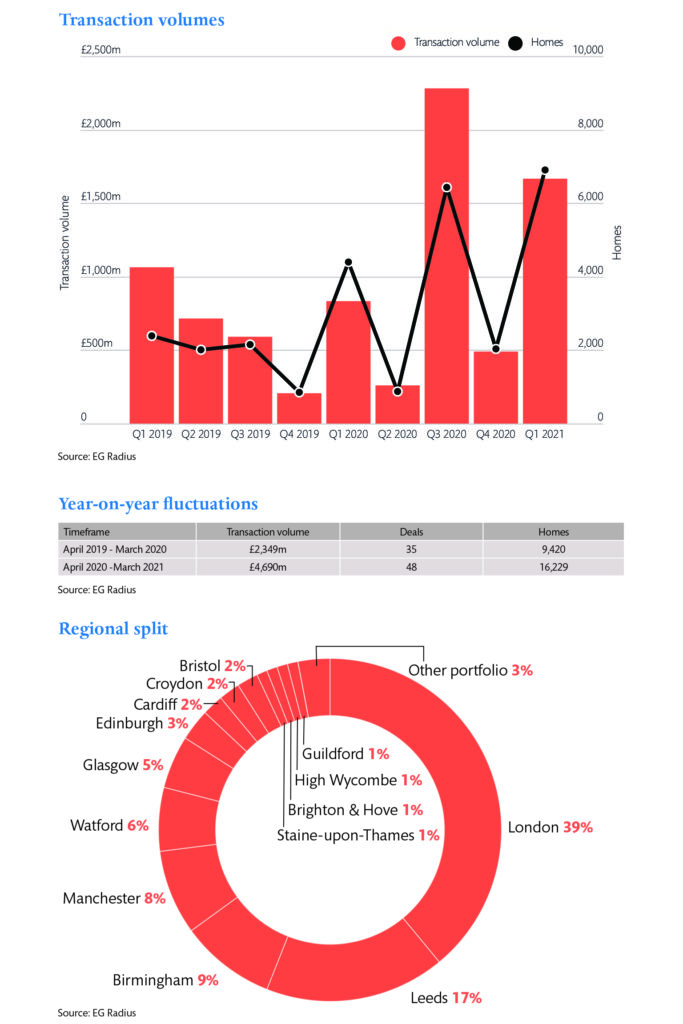

As fears for the future of the office and ailing high streets grow, the case for residential investment has never been stronger. While a year of lockdown saw transactions in most areas of commercial real estate put on ice, investment in the UK’s burgeoning build-to-rent sector doubled to £4.7bn.

EG Radius recorded 48 completed deals in the 12 months to the end of March, totalling 16,229 homes. This compares with 35 deals across 9,420 homes worth a combined £2.3bn in the previous 12 months.

Momentum continued throughout lockdown and into the new year, with some £1.7bn recorded in the first quarter of 2021. That marks the second-highest quarterly investment total on record, with the largest number of homes at 6,906. Investor appetite now looks set to continue, with billions targeting the sector and funds closing in on major landmark deals.

Buyers stick to the capital

More than half of investment in BTR over the past year (53%) was concentrated in London, through a mix of portfolio deals and high-value standing-stock acquisitions. These deals funded 39% of the total homes, with a further 34% across Leeds, Birmingham and Manchester combined.

Across the board, some 16% of capital committed was through portfolio deals, a slight dip on 20% a year earlier. Acquisitions of built assets surged to 35% of funds, from just 1% over the same period a year earlier.

Completed stock consistently quotes core yields of 3.5-4.5%. This dips lower in London, as seen in QuadReal’s £570m acquisition of Realstar’s 1,335 portfolio at a 3.6% yield, compared with the regions – for example, with Aberdeen Standard Investment’s Clarendon Quarter in Leeds at a 4.25% yield.

The biggest purchase of the year was AXA IM’s £800m investment of Dolphin Square, comprising 1,233 homes in Pimlico, SW1. Other significant deals included Long Harbour’s £156m forward-funding commitment for 315 flats at Berkeley Square Development’s Berol Yard in Tottenham Hale, N17, backed by a £120m debt facility from Wells Fargo.

Long Harbour has subsequently exchanged to acquire Capital & Regional’s The Mall in Walthamstow, in a deal that will see the investor expand into direct development. The purchase was made from Long Harbour’s £500m joint venture with a Canadian pension fund, which is weighted 70% to the capital.

“The pandemic has demonstrated the resilience of the sector, which is something that we have always talked about, but maybe didn’t have hard, tangible facts on,” says Rebecca Taylor, managing director of BTR at Long Harbour.

Those facts are now clear to see in Knight Frank’s 95% of rents collected from 22,000 tenants in the first three months of this year, or in listed landlord Grainger’s 89% occupancy and 98% rent collection for the six months to the end of March.

But, London’s story has had “two tales”, Taylor adds. While zone one and two locations have seen rental squeeze, there is continued demand for outer London and commuter areas. However, the city also has a high barrier to entry.

“We haven’t seen price drops on land or access to land, and we are still competing against the develop-to-sell model. It’s still quite a difficult sector to unwrap in London,” she adds. Further concerns over planning have been raised by groups including the British Property Federation, amid fears that these hurdles could dampen investment into the capital despite demand from renters.

“There has been maybe a miscommunication when people see premium product – they think that means premium returns and I think there is still an education piece for planners and the Greater London Authority, that it’s a stable income not a profit-on-cost model,” adds Taylor. “That education piece in terms of planning, clawback, section 106 is something that the sector is positioning ourselves for.”

Stabilised stock attracts attention

Long Harbour is a long-term investor, typically holding assets in a fund for 20 years. However, last year, as a seven-year fund came to an end, it sold the 129-flat Skyline in Manchester to L1 Developments after interest from several investors.

“We saw those traditional funds starting to reallocate funds and they wanted to get into standing stock residential,” says Taylor. “Last summer we saw an increase in appetite for that kind of stock and I’m sure that will continue as specifically designed BTR stock starts to come on to the market.”

Anticipating new acquisition opportunities in the wake of the pandemic led Canadian developer investor Realstar to pitch a near-£600m portfolio last summer.

“Our investors looked at the valuation and said it is a good time for us to think about recycling capital, given what new opportunities may present themselves coming out of the pandemic,” says Ryan Prince, vice-chairman at Realstar and founder of its BTR platform Uncle. “This was a good example of an extraordinary event.”

Realstar brought the 1,335-flat completed portfolio to the market in July and completed the £570m deal in just six months, following significant interest from domestic and international funders.

“The blue-chip universe of investors would come as no surprise. It was a large-core, core-plus portfolio, it required a lot of equity and therefore there was a range of large, institutional, pension fund investors,” says Prince. That risk profile opened the way for new movers in the sector, as investors from the UK, Europe, Asia and North America closed in.

“We always place certainty of execution pretty high on the list, although we had one group that was highly credible but hadn’t actually pulled the trigger on anything large of this nature in this asset class,” says Prince.

Having completed the Project Harmony sale, Realstar is on the hunt for new acquisitions. During the period it completed a £100m acquisition at HUB’s Wembley Link and has since signed two more deals, conditional on planning.

Prince is also scoping out cities for UK expansion. “I like the dispersion, the choice, the different nature of the buildings,” he says. “That’s how we have been approaching it and trying to pick off locations where we can find the sweet spot – that Goldilocks bit where we can afford the deal and yet it is convenient and an appropriate product for the customer.”

BTR movers, shakers and new players

Over the past 12 months, 41 investors have committed funds to BTR, double the number that did so in the previous year.

Delph Property’s new BTR brand, Kooky, was the most prolific purchaser, scooping up five sites in a fresh strategy that saw it opt to acquire completed assets around London from developers ready for occupation. Aberdeen Standard Investments, Grainger and Federated Hermes’ Hestia, backed by BT Pension Scheme, also each completed three acquisitions during the period – each with further schemes under offer.

During lockdown, Pension Insurance Corporation completed a debut BTR deal with the £130m forward funding of Muse and Network Rail’s New Victoria in Manchester. This year has also seen a debut investment from DWS and a return to UK BTR for Patrizia with new client mandates funding schemes in London and Birmingham.

Gerald Eve partner Bobby Barnett notes the variety in capital sources targeting the sector today. “Large-scale investment into the UK residential market seemed to start with largely defined-benefit pension money using specialist vehicles, cautiously forward purchasing purpose-built city centre blocks for the higher-end rental market to achieve long-term income streams with a perceived inflation hedge,” he says.

But as developers add sub-sectors such as single-family housing, affordable housing, mid-market and small blocks to the mix, different buyers are coming to the table. Barnett says “a broader and deeper pool of capital with private equity is looking at development and delivering fully let stabilised assets to the market as well as bulk purchases from housebuilders”.

He adds: “Alongside institutional investors, property companies, sovereign wealth, family offices and now balanced UK real estate funds are all looking to allocate to the sector.”

Goldman Sachs has taken the leap into single-family housing with Sigma Capital and Gatehouse Bank’s Thistle portfolio. Meanwhile, Canadian fund AIMCo is building a portfolio of regional sites to develop in joint ventures, including three sites with Ridgeback and a £75m equity deal with Platform_ in the works. As schemes progress, the sector will no longer be considered alternative, says Barnett. Proof of rental returns and greater data from operational assets will support underwriting, giving confidence to the next generation of investors.

Gearing up for new investment

As investors pile into the sector, developers are also adjusting their businesses to take advantage of the BTR boom.

Developer London Square has pivoted its business to gear up for BTR and is in the process of setting up a joint venture with Moda Living for a 760-flat scheme at Royal Mail’s Nine Elms site. Having committed £1bn to the regions, Moda Living has now set its sights on the capital to expand its 8,000-home pipeline, with a number of schemes in the works, including a £300m development in Kingston with Apache Capital Partners. Regal London has also shifted its attention from smaller, luxury, private-sale assets to larger regeneration with mixed tenures in the outer boroughs.

New appetite for single-family housing has seen L&G launch a dedicated Suburban Build-to-Rent business, which recently appointed Grainger acquisition director Tom Henry to lead on new purchases. Residential developer Pitmore has poached from Knight Frank and CBRE to drive forward its rental strategies, including major ventures with Goldman Sachs.

Those businesses are readying for continued spend from seemingly bottomless cash piles. EG data estimates more than £6bn targeting UK BTR through funds already secured and active fundraises.

At the start of April, AXA IM announced it had raised €800m (£691m) in the first close of its fifth generation development strategy – targeting BTR and offices in Europe. The equity was raised from five Asian, North American and European institutions that see opportunity for BTR through converting old office stock and new-build development.

Federated Hermes’ Hestia platform is also in talks with new investors with a plan to deploy £1bn in cash in under three years.

Macquarie Bank is also planning for its first BTR deals, looking to raise £1bn from investors in a tie-up with the founders of Essential Living, and Greystar has yet to tap the £750m dedicated to BTR closed in 2019.

While fund managers continue to court prospective investors, the pipeline of schemes is swelling. And with a growing hit-list of cities and sub-sectors, we can expect more deals and greater diversity in BTR investment outside of lockdown.

To send feedback, e-mail emma.rosser@eg.co.uk or tweet @EmmaARosser or EGPropertyNews