First in, first out. The upswing in North America is gathering momentum fast post-2008. Investment volumes have risen across the continent by 14.3% over the past 12 months and as most US regions prepare for a year of growth, the effect on real estate will be significant.

At city level, the majority are experiencing economic expansion (apart from those dominated by the energy sector), which is fuelling both the commercial and residential sectors, according to Cushman & Wakefield. The Canadian market is faring well against the backdrop of an economy bolstered by domestic pension funds during the global financial crisis. In short, things are looking pretty swell in the US of A and this year looks set to be one of optimism. But beware blind faith – there are still danger zones.

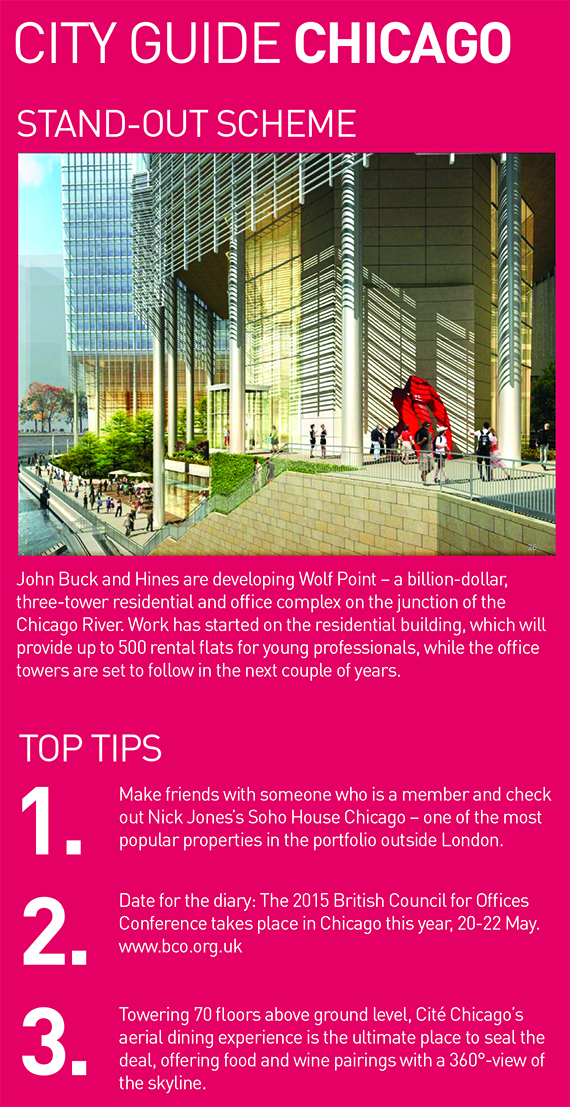

Commercial hotspots

In the offices market, double-digit rent growth is forecast for cities including San Francisco, New York, Seattle and Boston, according to C&W’s 2015-2016 Global Office Forecast. Even in the worst-performing cities of Los Angeles and Washington DC, office rents are predicted to rise this year and next. In Canada, office vacancy rates stand at less than 10% and developers are adding more than 20m sq ft of new space to the market – 5m sq ft of which will be delivered in Toronto alone by 2017.

In the retail sector, prime rental values in the Americas were ahead of those in the rest of the world at 5.8%, according to C&W, with North America fuelling the expansion. New York’s Fifth Avenue was named the world’s most expensive retail street, and San Francisco’s Union Square the world’s leading retail growth location.

Residential hotspots

The homeownership rate in the US dropped to 64.7% as of 30 June 2014 – the lowest since 1995. As a result, multi-family (PRS) residential across the US has become increasingly prevalent and saw 18% growth over the last 12 months. Furthermore, the US accounted for 69% of all activity in the sector across the globe between 2013 and 2014.

In terms of residential trends, New York is an interesting indicator of possible global patterns. This is, perhaps, a wake-up call for the luxury residential sector, at least in the Western Hemisphere. Prices for luxury co-ops and condos in Manhattan fell by 11% last year, according to Corcoran, a New York residential agency.

Andy Schofield, head of research at TIAA Henderson Real Estate, points out the pattern of rising prices, which is fuelling a continued shift from prime central Manhattan properties out to the New York suburbs, is already being emulated in London, where the heat has come out of the prime central area and shifted to zones 2 and 3. Adam Challis, head of residential research at JLL, believes a resurgent greenback will curb some international buyers, an important factor in Manhattan’s recovery.

For house price growth, Florida remains the state at the top of the Forbes Best Buy List. Orlando sits at number four with average house prices standing at $187,568 (£121,508), followed by North Port ($223,523), West Palm Beach ($260,846), and Jacksonville, where prices hover just under $200,000.

Growth areas

San Francisco remains the Mecca for the global tech set. The city has seen 37% rental growth in the past five years, and as long as the TMT sector continues to perform well this is considered one of the (albeit riskier) growth areas.

Hotels have also been earmarked as a growth area. Despite hospitality remaining the smallest global investment sector, according to C&W’s International Investment Atlas Summary, the sector saw a 24% surge in activity last year. The report states that room for growth in 2015 is significant in North America, with New York, Chicago and Miami topping the list of key cities for this sector.

Risks and challenges

Cities dependent on single sectors have been highlighted as being most at risk. Despite a strong performance and impressive growth predictions in San Francisco, this has been raised as a concern due to the city’s increasing reliance on the tech sector and TMT occupiers. Following the oil price crisis, Houston is a prime example of what can happen in a city so reliant on one sector (see main feature, overleaf). Uncertainty in the run-up to the next presidential election in November 2016 might not be an issue just yet, but could start having an effect on investor confidence at the start of next year.