What does it say about a market when two of the largest deals of the quarter weren’t even in ‘Central’ London?

What does it say about a market when two of the largest deals of the quarter weren’t even in ‘Central’ London?

While it is still slightly too early to call take-up for Q2, there is no need to wait until the final numbers are in to know which emerging sub-market stole the show this quarter – Stratford.

The FCA and Transport for London finally completed their long-anticipated pre-lettings at Stratford’s International Quarter, which collectively are just shy of 700,000 sq ft. Stratford is increasingly now being classed as part of the Central London office market – at least where occupiers are concerned.

Agents still seem undecided whether it belongs with those core figures, but one thing they all agree on is that it can’t be ignored. At present EGi doesn’t even include this market in our London office market analysis, but these mega deals are making us wonder if we should.

Space is running out in the centre. In Q1 the market saw supply in London decline further and availability contract to 5.8%. We also saw more office space snapped up prior to completion.

At the end of the quarter only around 400,000 sq ft of the 1.1m sq ft which completed still remained available. So what now?

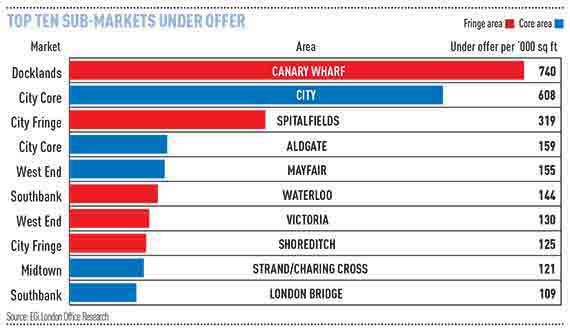

While the figures are still being collated for Q2, a quick look under the bonnet shows 3.5m sq ft of space is under offer, the highest we’ve seen since our records began in 2004.

The winners are those on the periphery rather than the core. Five of the top 10 sub-markets by space under offer were fringe markets. Over this quarter Canary Wharf overtook the City sub-area, with a massive total of 740,300 sq ft under offer. This included 388,800 sq ft under offer at 10 Upper Bank Street, E14, to Deutsche Bank, which recently completed. The bank considered Canary Wharf as an ideal spot for relocating some of its other offices, including space at 6-8 Bishopsgate, EC2. With average rents in the £40 per sq ft region, Canary Wharf presents occupiers with an opportunity to escape rising rents to the west, though rents east are on the rise.

The winners are those on the periphery rather than the core. Five of the top 10 sub-markets by space under offer were fringe markets. Over this quarter Canary Wharf overtook the City sub-area, with a massive total of 740,300 sq ft under offer. This included 388,800 sq ft under offer at 10 Upper Bank Street, E14, to Deutsche Bank, which recently completed. The bank considered Canary Wharf as an ideal spot for relocating some of its other offices, including space at 6-8 Bishopsgate, EC2. With average rents in the £40 per sq ft region, Canary Wharf presents occupiers with an opportunity to escape rising rents to the west, though rents east are on the rise.

This quarter we can really see demand growing in office development areas such as King’s Cross, Stratford, Waterloo and Victoria, as well as well-established Canary Wharf and City fringe areas. And we have seen record-breaking rents in the West End such as 8 St James’s Square, SW1, where lettings reached £185 per sq ft in March, and in the City this May, with the first letting outside of the City’s skyscrapers to stray to £75 per sq ft at 100 Cheapside, EC2. Although these record lettings have been unique rather than the trend for their area, with rents rising and demand growing, the concept of a ‘Central’ London office market location can only continue to blur.

Victoria Bajela is head of London offices research, EGi