Birmingham is flying high. Office take-up topped 970,000 sq ft in 2015, 40% above the five-year average, and demonstrating that the UK’s second city is finally living up to its potential as an office location.

Birmingham is flying high. Office take-up topped 970,000 sq ft in 2015, 40% above the five-year average, and demonstrating that the UK’s second city is finally living up to its potential as an office location.

HSBC’s choice of Birmingham as the home of its retail banking operation grabbed the headlines. The bank’s decision to take 210,000 sq ft at Arena Central Development’s eponymous Arena Central scheme was significant not only because of the size of the deal, but what it signifies.

“The rise in take-up is phenomenal, but perhaps what is most significant is that 30% of that was inward investment,” says Bilfinger GVA senior director Charles Toogood.

Agents predict the city’s ongoing investment in infrastructure and new grade-A product will place it in prime position to attract further relocations. According to research by CBRE, occupancy costs in Birmingham now stand at £46 per sq ft, compared to £180 per sq ft in London’s West End.

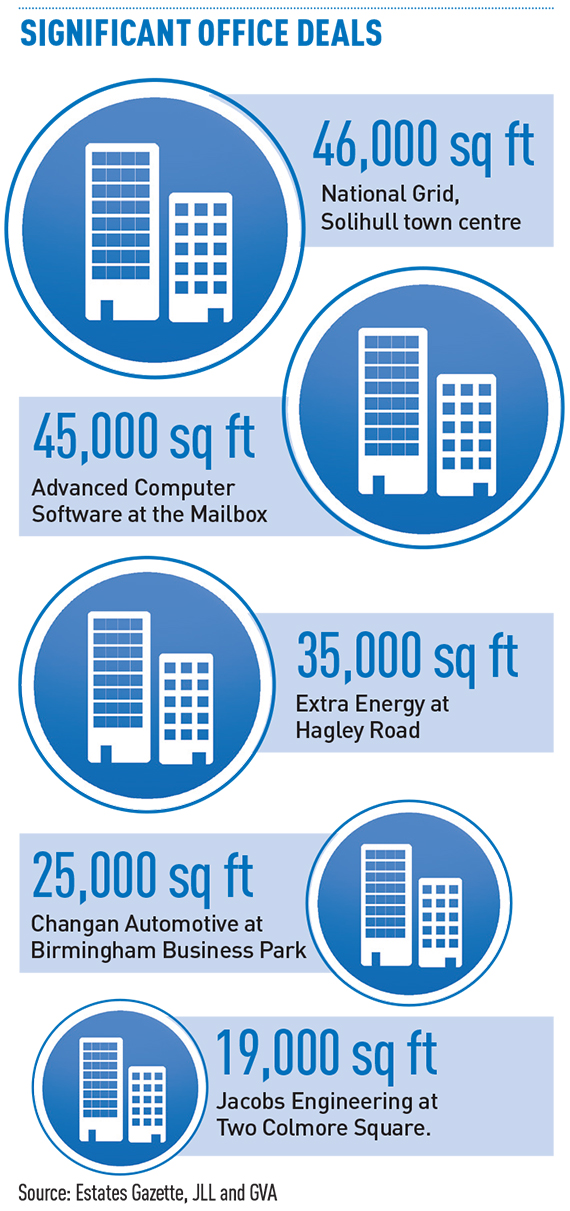

Around 1m sq ft of new office space is under construction in Birmingham. Although the two key regeneration projects – the 2.3m sq ft Arena Central and Hermes Investment Management’s and Argent’s 1.8m sq ft Paradise – won’t deliver until 2018, there is around 370,000 sq ft of refurbished space due for completion by the end of the year.

David Tonks, head of Cushman & Wakefield’s Birmingham office, says: “However you look at it, Birmingham is a greater proposition now than ever before.”

But is the city’s success to the detriment of other West Midlands locations?

On the face of it the answer is no. The region’s out-of-town market also celebrated a record year. In 2015, the M42 corridor (spanning junctions one to seven) racked up 490,000 sq ft of deals – also 40% above the five-year average.

The biggest deal was Interserve’s sale and leaseback of 114,000 sq ft at International House in Solihull.

Demand is strong across a range of sectors, particularly the likes of automotive and aerospace. “There is no reason why these levels of take-up can’t remain ahead of their long term average – the only challenge is a shortage of stock,” says JLL’s Jonathan Carmalt.

Market forces ought to be encouraging developers to at least consider pushing the button for speculative development.

But developers remain wary. At Blythe Valley Business Park, IM Properties is prioritising refurbishing unoccupied stock, including a 58,000 sq ft building it is branding One Central Boulevard. The developer is also preparing an outline application for the entire site, which will incorporate 880,000 sq ft of offices.

IM’s Lewis Payne explains: “We’re gearing up to get everything in place and getting to a position where speculative development is becoming more likely, but I’m not sure it will happen this year.”

The longer developers hold back, the greater the danger the market will lose out on potential occupiers as stock continues to diminish.

The fear of missing the boat has led to a number of regional cities thinking more creatively about new office development. Rather than waiting for funding streams and viability to improve, local authorities are stepping into the breach.

Wolverhampton City Council invested more than £10m in bringing forward its mixed-use Interchange project. The council moved into the scheme’s first building in 2012 and in December 2015 its partner Neptune Developments completed building i10, the only grade-A office space in the city.

Deals are in solicitors’ hands for much of the 28,000 sq ft of office space, including one inward investor.

“The level of interest has surprised us and led us to start planning to deliver further speculative office space,” says Neptune Developments’ Rob Mason.

Local agent Bulley’s let and sold almost 300,000 sq ft of offices across Wolverhampton in 2015, at least twice the level of the previous year. Agents report significant demand from the automotive sector, linked to Jaguar Land Rover’s 1m sq ft new engine plant, i54, yet Wolverhampton also has a strong record in insurance and financial services.

The council’s strategic director, Tim Johnson, says: “We had to step in to capitalise on occupier interest through a new commercial quarter. We can be attractive to occupiers who want locational advantages but aren’t in the market for central Birmingham rents.”

A similar strategy is in place in Coventry which has long punched well below its weight as an office location.

As with Wolverhampton, Coventry’s city centre has been overshadowed by a far stronger out-of-town office market and is chronically short of decent stock.

Jonathan Moore, of local agent Shortland Penn & Moore, says: “Demand is good across the board, but unless Coventry can deliver new city centre office space, it faces losing out on potential occupiers.”

With an historic headline rent of £18 per sq ft, it is little wonder the private sector has been unwilling to provide new space. Yet intervention by the city council has prompted the development of the 3m sq ft mixed use development, Friargate (pictured above).

Coventry City Council’s Martin Yardley says: “In establishing a new business district, we need to demonstrate things are happening. We are having our own 160,000 sq ft building and are very keen to get the next office building out of the ground.”

Developer Friargate Coventry is about to submit a planning application for the second building of around 130,000 sq ft and is agreeing heads of terms with the RICS for a 35,000 sq ft prelet.

Yet Friargate will need more space prelet before committing to construction. The council is keen the scheme doesn’t stall in the meantime. Yardley is talking to the developer about how it might use its £50m Coventry Investment Fund to accelerate development and be able to offer occupier-ready buildings.

“It is critical that building comes out of the ground,” says Yardley. “It might be that we can underwrite the space and if we can’t rent it, use it ourselves.”

That strategy has also been adopted by Stoke-on-Trent City Council to kick-start its new 1.2m sq ft office quarter, Smithfield. The council signed up for the first two office buildings to stimulate development in a town centre which has no established office district.

Developer Genr8 completed two office buildings last December. The council is in the process of moving public sector staff into one building and after deciding the second, 80,000 sq ft, second building is surplus to requirements, has appointed agent Bilfinger GVA to let it.

“This is a game changer for Stoke”, says Bilfinger GVA’s Andrew Venables. He says having a building ready to occupy offers an advantage when competing for footloose occupiers and adds: “With rents of £18 per sq ft and the possibility of flexible terms, we already have three serious enquiries.”

2016 prospects

Can Birmingham’s office market maintain its take-up momentum and set more records in 2016?

Agents predict a strong start to the year, be it PwC rumoured to be committing to Paradise, or Pinsent Masons poised to take 45,000 sq ft at IM Properties’ refurbishment 55 Colmore Row, plenty of deals are in the offing.

According to JLL, grade-A stock is down to just 323,000 sq ft and occupiers will be keen to sign up early for prelets to secure the right building.

Whether take-up can nudge the 1m sq ft mark again, may require another major relocation of HSBC’s ilk.

“New prelets are likely to be around £32.50 per sq ft”, says Colliers’ Matt Long. “We were at that level pre- recession.”