The Midlands is the region most starved of shed supply, postcode analysis by EG data shows.

Using Valuation Office Agency data to ascertain overall stock levels, EG has been able to calculate availability rates for industrial supply nationwide, with the East Midlands showing a 7.9% supply rate against a national average of 12.4%.

Over in the West Midlands, where supply is a little less constrained at 9.3%, active demand over the past 12 months or so leaves the region with the lowest amount of stock remaining at present take-up rates, with supply set to run out in just 1.4 years.

The figures include available units which at present are rated below the new minimum energy efficiency standard to be introduced from next April – meaning areas which are presently constrained will become even more squeezed once units deemed unfit for purpose drop out of the supply pool.

London, along with the West Midlands, boasts the highest proportion of new-build or refurbished standing availability – both at around 25%. By contrast, just 11% of the East Midlands’ standing available stock is newly built – only Wales and the East of England are poorer in this regard.

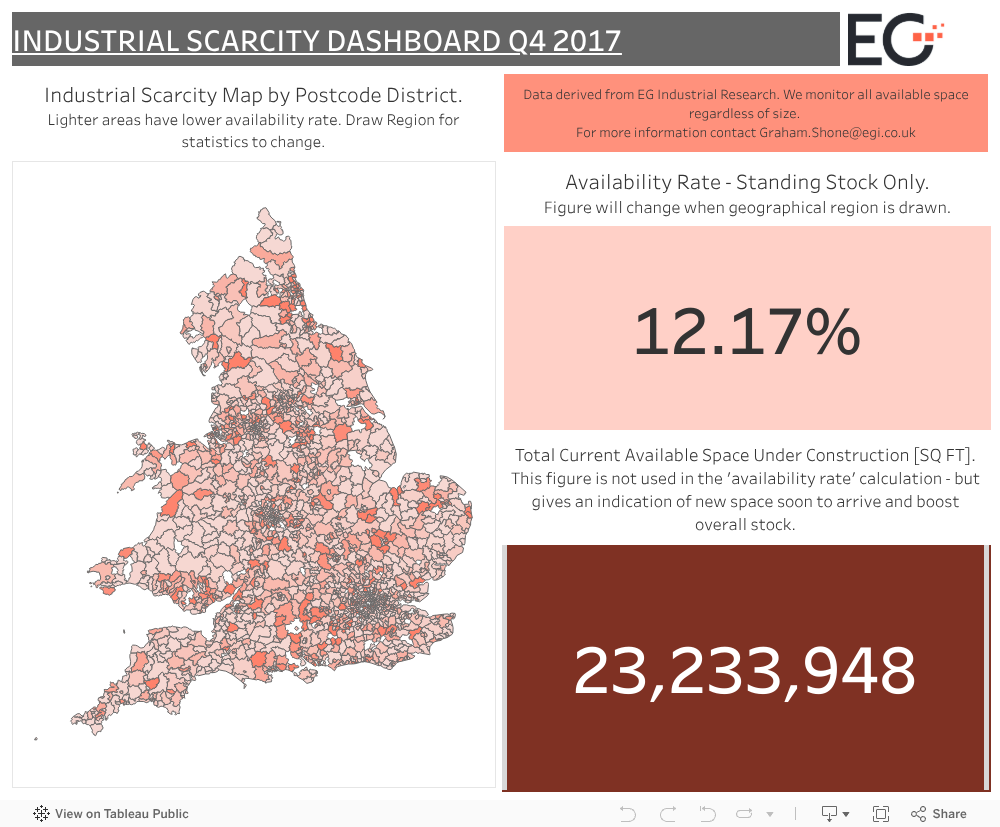

Our interactive dashboard allows you to draw your area of interest and assess the current supply rate, as well as the total amount of under-construction space available at present.

To send feedback, e-mail graham.shone@egi.co.uk or tweet @GShoneEG or @estatesgazette