On 11 April the Cambridge and Oxford rowing teams will take to the water to fight for victory. For one team a shining triumph, for the other a watery demise.

On 11 April the Cambridge and Oxford rowing teams will take to the water to fight for victory. For one team a shining triumph, for the other a watery demise.

Office agents watching from the banks of the River Thames might feel some level of kinship as the two cities’ markets slog it out to increase demand from high-tech tenants.

But while Oxford might have won the boat race 78 times to Cambridge’s 81 (with one draw), Oxford’s office agents could only dream of those sort of odds. With Cambridge pulling ahead in terms of rents, take-up and supply, can it ever catch up with its Silicon Fen rival?

On paper the two cities are similar. A population of around 110,000; an hour’s train ride from London; a thriving tech scene and world-renowned universities. All of which are driving thriving real estate markets.

But a damning report published by the university, the city’s LEP and the city and surrounding district councils showed that despite the wealth of assets in Oxford and the Oxfordshire area it had underperformed and failed to reach its full potential when compared to other internationally renowned areas such as Massachusetts Institute of Technology, Stanford and, critically, Cambridge.

Furthermore, a recently published Oxfordshire Innovation Engine report showed Oxford’s growth was some way behind its East Anglian neighbour – having grown at the same rate as Cambridge between 1997 and 2011,

it has been constrained by transport infrastructure and underdeveloped business networks.

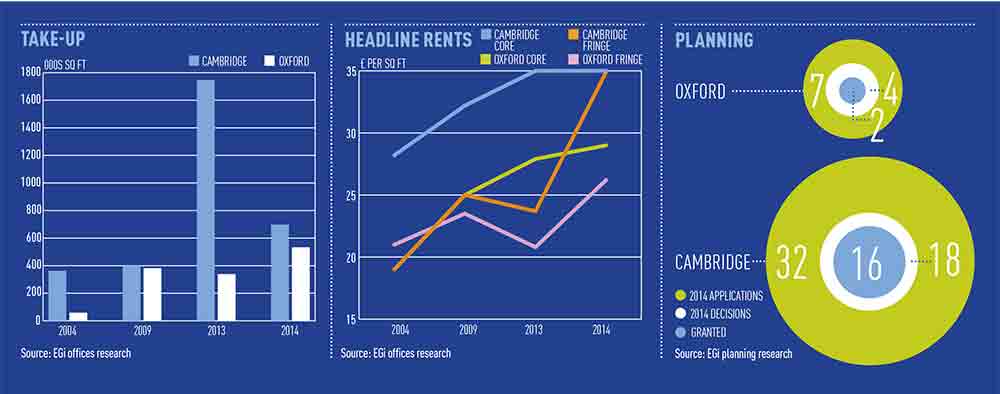

A quick look at take-up confirms this. While office space signed for is rising in both cities, Oxford’s total is just three-quarters that of Cambridge, where nearly 700,000 sq ft of take-up was recorded last year, according to EGi data – a 75% rise on five years ago and double that seen 10 years ago.

A quick look at take-up confirms this. While office space signed for is rising in both cities, Oxford’s total is just three-quarters that of Cambridge, where nearly 700,000 sq ft of take-up was recorded last year, according to EGi data – a 75% rise on five years ago and double that seen 10 years ago.

The rise, according to Rob Sadler, head of Savills’ Cambridge office, is because of changing demand. “A decade ago the majority of take-up had been home-grown businesses, spun off from the university and mostly R&D related. But in the past year we have seen such names as Apple and Spotify wanting to put a flag into Cambridge.”

He says they like Cambridge for the obvious reasons – an educated workforce, close connections with the university and proximity to London.

And yet, despite all those qualities, Oxford has yet to pull in the same kind of international occupier interest, admits Jon Silversides, partner in Carter Jonas’s Oxford office.

Take-up is rising, reaching an all-time high of more than 533,000 sq ft last year – up 60% on 2013 and nearly 10 times the 2004 total – but Silversides adds: “The large movements have been relocations of existing companies within the county – for instance Smeg taking 40,000 sq ft in Abingdon.”

Are occupiers simply favouring one of the cities on cost? Oxford’s rents have seen double-digit growth over the past five years, with many rising by 16%, but at £26 per sq ft last year they are still trading at a discount to Cambridge’s headline rent of £35 per sq ft.

Both cities are forecast to see office returns outstrip the rest of the UK, according to a recent report by Carter Jonas. Against the UK’s total return figure of 6.8% per annum, Cambridge is forecast to see a total return of 9.3% pa and Oxford 8.1%. A lack of supply will help keep that growing, especially into the science and business parks, which contain most of the available space.

So maybe it is a difference in opportunity? The figures don’t seem to agree, as neither city has supply to last much longer than a year, at present take-up rates. Both have less than 150,000 sq ft of new or refurbished space and are crying out for development, and that’s the rub. Neither city has the strongest reputation for development. Constrained by historic centres in the core and the green belt around the edges, commercial developers compete with higher value housing developers for land.

Cambridge saw 32 applications in 2014, 16 of which were granted – a success rate of 50%. Oxford, meanwhile, saw just seven applications over the same period , only two of which were granted, or 29%.

So it is ironic that Cambridge agents are actually more vocal about their discontent with their council.

“Planning has always been difficult,”

says Will Mooney, partner at Carter Jonas Cambridge. “In a city with close to zero unemployment in real terms, there is just not the need to attract more people, and there is protectionism too, against development and the people coming with that. AstraZeneca’s move means many thousands of people coming in one hit – where is the housing and infrastructure to support that?”

Head 84 miles west and in Carter Jonas’ Oxford office, Silversides says Oxford is not restrictive, it is just hampered by lack of opportunities.

Nick Berrill, commercial director, Savills Oxford, adds: “Oxford council is pro- development – for instance the West End Area Action Plan – and there are some big schemes planned outside the city centre.”

While Cambridge seems to be pulling ahead of its old rival – particularly through a flurry of international lettings – the supply squeeze in both may shake up the fringe markets, which could allow Oxford to catch up.