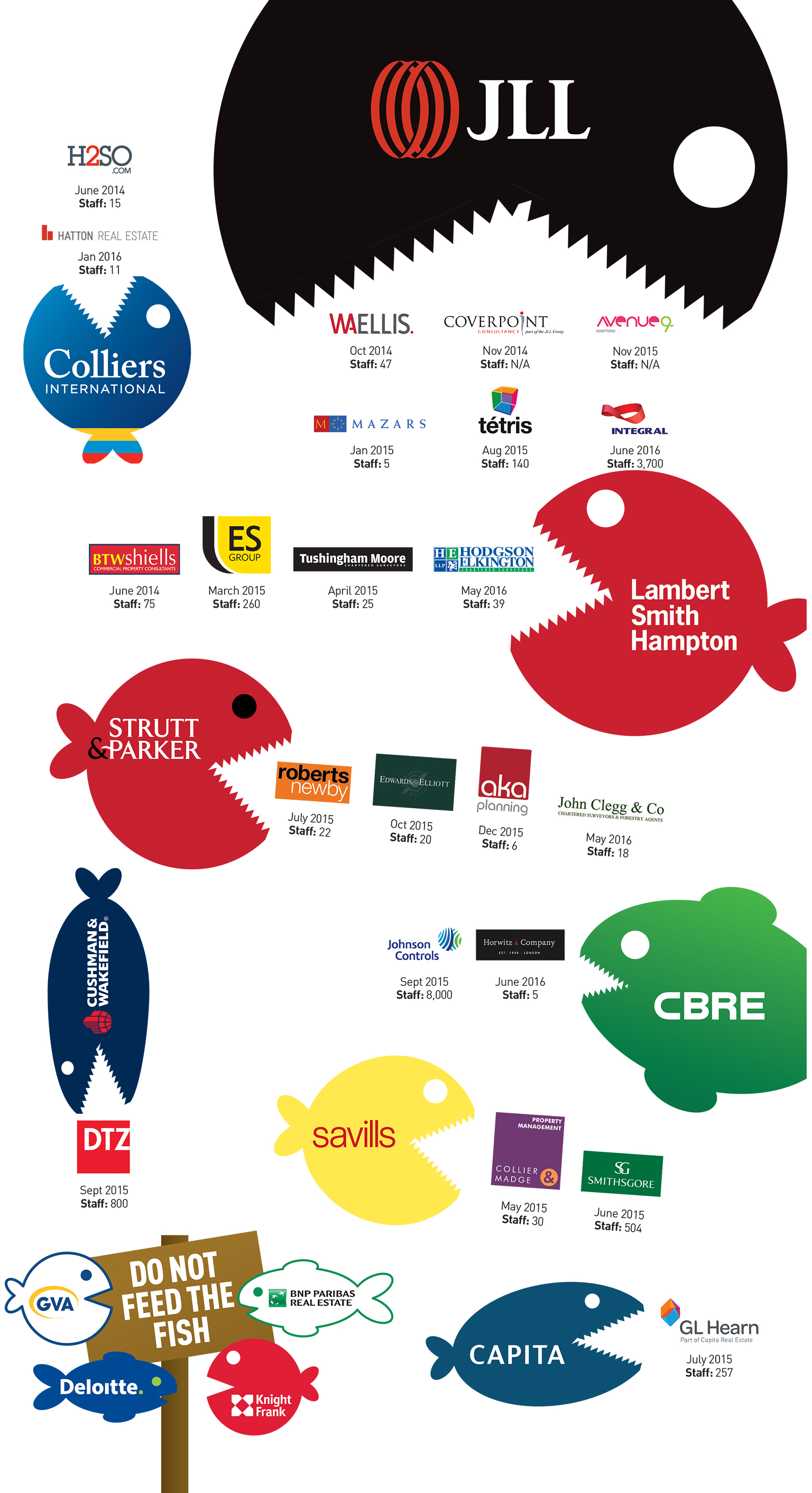

This week’s acquisition by JLL of property maintenance group Integral and last week’s sale of niche luxury retail agency Michael Horwitz to CBRE are the latest in a long line of advisory firm mergers.

Since the beginning of 2014, there have been 22 UK mergers and acquisitions by the country’s top 12 advisory firms – and they are not over yet.

Most of the top agency firms have bought rivals and been part of steady M&A activity driven by the need to increase and diversify their offerings.

Mark Ridley, chief executive of Savills, says the desire from clients for an increasing range of multi-sector services will ensure M&A activity continues.

“I think mega-mergers are far less likely, but with the squeeze that has happened in mid-size firms across the UK and Europe, acquisitions will probably continue,” he says.

Ridley adds that there has been an eruption of smaller, niche firms as well.

The time might be ripe for these boutique agencies, but they need to be careful that they are “niche enough” to ensure they differentiate themselves from larger firms, says Nigel Shilton at Deloitte Real Estate.

“They might find it increasingly difficult to complete if they are not specialist enough, especially with large clients that are looking for more international-based advisers,” he says.

“Mid-sized firms will continue to be acquired, especially if they have a particular strength in a regional sector.”

A cooling market could also drive acquisition activity.

Ezra Nahome, chief executive of Lambert Smith Hampton, says large firms have been growing through acquisitions for the past 20 years, but the number of medium-sized

companies is also increasing.

He stresses the importance of such firms creating their own identity. “Some firms lose their way and some don’t create this identity in ways they should, which makes them more prone to be consolidated by firms where there is better clarity on offerings in the marketplace,” says Nahome.

He adds that LSH’s acquisitions strategy is to provide a range of in-depth services across various regions and sectors, but he warns of the dangers of acquiring companies without integrating them.

Companies are also increasingly looking to secure recurring income through acquisitions rather than seeking traditional transactional income.

“As markets get tighter, sometimes there can be an

economic imperative for businesses to join forces,” says Nahome.

“With some of our larger competitors’ strategy focused on providing a significant depth of service across a global platform, sometimes with that there can be weaknesses about quality of service and client management.”

Nahome adds: “Experience has shown us that acquisition is all well and good, but the integration of these companies is fundamental to success. That, for me, is a big red flag to a lot of businesses out there.”

Ridley agrees, saying that growth is not an “arms race” but about giving clients choice.

In the future, companies may also need to take a long-term view about whether M&A works for them.

Knight Frank has not acquired any companies recently and says M&A activity is not in line with its strategy.

Group chairman Alistair Elliott says the company prefers to recruit teams and individuals to maintain its independence – including Deloitte’s 48-strong asset and property management teams.

“We are a global independent partnership – there isn’t another one,” he says.

“While there are a series of other businesses that have a global footprint, that may work for them, they are not partnerships.

“There is cultural difference within our organisation born out of being a partnership. We are financed internally and this ensures we are in control of our own destiny.”

To send feedback, e-mail Shekha.Vyas@estatesgazette.com or tweet @shekhaV or @estatesgazette