The insatiable demand for online retail coupled with London’s growing population – predicted to exceed 10m by 2031 – means industrial land needs to be protected. A new report from industrial REIT SEGRO and planner Turley, Keep London Moving, shows how it is crucial to halt the loss of the capital’s industrial land to other uses. Change of use to residential, together with the growth of e-commerce, is driving the demand for industrial land even further.

SEGRO chief executive David Sleath says: “There needs to be a thorough review of industrial land designation, which recognises the requirements of urban logistics operators to be located where they are able to respond to last-mile activities. We need to ensure the industrial and logistics sector has a voice within London policy decision-making to ensure that the rapid loss of industrial land is reversed and intensification of industrial and logistics uses is possible when practical.” Read more from David Sleath >>

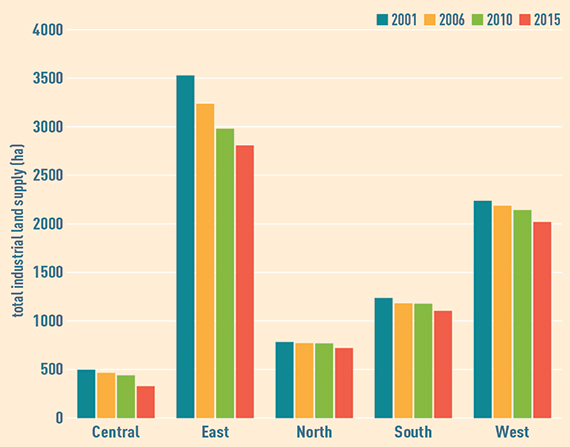

Industrial land supply by sub-region 2001-2015

The supply of industrial land has been contracting since 2001, affecting every sub-region of London.

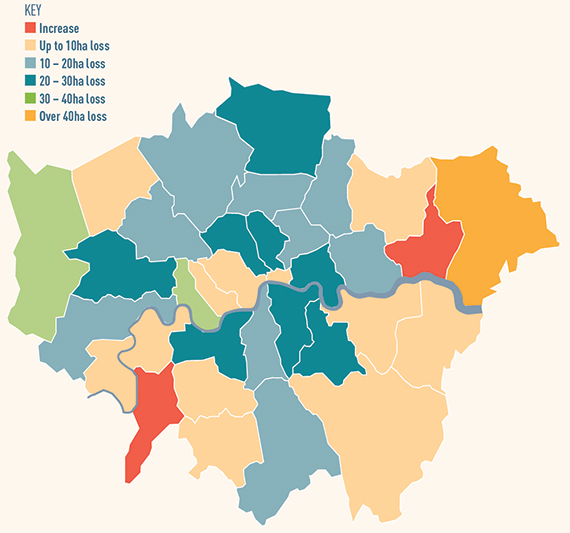

Absolute change in industrial land supply 2010-2015

The London Plan includes provision for the managed release of 37ha of surplus industrial land annually from 2011 to 2031 across the capital. The Greater London Authority has identified the greatest opportunity for release in east London and parts of inner west London, with more limited scope in north and outer west London.

Historic absolute change in industrial land supply by sub-region 2001–2015 (ha)

2001-06

2006-10

2010-15

2001-15

Central

-32

-26

-111

-169

East

-129

-258

-172

-721

North

-12

-3

-48

-63

South

-55

-5

-74

-134

West

-51

-45

-124

-220

London

-440

-337

-528

-1,305

London industrial land loss 2031 target and pipeline (ha)

Industrial land

Industrial land loss from 2010

Equivalent number of Park Royals lost

2010

7,505

n/a

n/a

2031 target

6,700

805

1

Pipeline loss (20 years)

6,147

1,358

2

All eight boroughs in the Park Royal/A40/Heathrow area are likely to exceed their targeted release by 2031. Five are already at the target release level.

Historic absolute change in industrial land supply by sub-region 2001–2015

Total industrial land supply 2020 (ha)

Total targeted loss in industrial land 2011 – 2031

Targeted annual loss of industrial land 2011 – 2031 (ha)

Annual actual loss of industrial land 2010 – 2015 (ha)

Annual potential pipeline loss of industrial land (ha) 20 years

The insatiable demand for online retail coupled with London’s growing population – predicted to exceed 10m by 2031 – means industrial land needs to be protected. A new report from industrial REIT SEGRO and planner Turley, Keep London Moving, shows how it is crucial to halt the loss of the capital’s industrial land to other uses. Change of use to residential, together with the growth of e-commerce, is driving the demand for industrial land even further.

SEGRO chief executive David Sleath says: “There needs to be a thorough review of industrial land designation, which recognises the requirements of urban logistics operators to be located where they are able to respond to last-mile activities. We need to ensure the industrial and logistics sector has a voice within London policy decision-making to ensure that the rapid loss of industrial land is reversed and intensification of industrial and logistics uses is possible when practical.” Read more from David Sleath >>

Industrial land supply by sub-region 2001-2015

The supply of industrial land has been contracting since 2001, affecting every sub-region of London.

Absolute change in industrial land supply 2010-2015

The London Plan includes provision for the managed release of 37ha of surplus industrial land annually from 2011 to 2031 across the capital. The Greater London Authority has identified the greatest opportunity for release in east London and parts of inner west London, with more limited scope in north and outer west London.

Historic absolute change in industrial land supply by sub-region 2001–2015 (ha)

2001-06

2006-10

2010-15

2001-15

Central

-32

-26

-111

-169

East

-129

-258

-172

-721

North

-12

-3

-48

-63

South

-55

-5

-74

-134

West

-51

-45

-124

-220

London

-440

-337

-528

-1,305

London industrial land loss 2031 target and pipeline (ha)

Industrial land

Industrial land loss from 2010

Equivalent number of Park Royals lost

2010

7,505

n/a

n/a

2031 target

6,700

805

1

Pipeline loss (20 years)

6,147

1,358

2

All eight boroughs in the Park Royal/A40/Heathrow area are likely to exceed their targeted release by 2031. Five are already at the target release level.

Historic absolute change in industrial land supply by sub-region 2001–2015

Total industrial land supply 2020 (ha)

Total targeted loss in industrial land 2011 – 2031

Targeted annual loss of industrial land 2011 – 2031 (ha)

Annual actual loss of industrial land 2010 – 2015 (ha)

Annual potential pipeline loss of industrial land (ha) 20 years

Barking and Dagenham

475

-7%

-2

1

6

Barnet

115

-9%

-1

-3

0

Bexley

528

-9%

-2

-1

2

Brent

411

-6%

-1

-2

2

Bromley

136

-7%

0

-1

0

Camden

61

-8%

0

-4

0

City of London

5

0%

0

0

0

Croydon

180

-5%

0

-4

0

Ealing

534

-4%

-1

-4

3

Enfield

486

-7%

-2

-5

3

Greenwich

240

-21%

-3

-1

3

Hackney

74

-14%

-1

-4

0

Hammersmith and Fulham

172

-23%

-2

-7

3

Haringey

167

-14%

-1

-2

2

Harrow

71

-20%

-1

-1

1

Havering

510

-7%

-2

-13

1

Hillingdon

430

-6%

-1

-7

3

Hounslow

496

-3%

-1

-3

1

Islington

70

-7%

0

-5

0

Kensington and Chelsea

28

-7%

0

-2

0

Kingston upon Thames

116

-6%

0

0

0

Lambeth

96

-8%

0

-4

1

Lewisham

135

-25%

-2

-6

1

Merton

177

-5%

0

-2

0

Newham

563

-19%

-5

-3

3

Redbridge

72

-15%

-1

-1

0

Richmond upon Thames

48

-8%

0

-2

0

Southwark

170

-15%

-1

-5

0

Sutton

334

-3%

0

0

1

Tower Hamlets

180

-19%

-2

-4

3

Waltham Forest

214

-13%

-1

-3

1

Wandsworth

179

-23%

-2

-6

2

Westminster

19

-5%

0

-2

0

Projected population growth in London

Employment growth 2011-31

% employment growth 2011-31

Projected population growth 2011-31

Population growth 2011-31

Barking and Dagenham

-1,000

-2%

71,920

38%

Barnet

32,000

23%

100,767

28%

Bexley

11,000

15%

39,076

17%

Brent

27,000

24%

58,536

19%

Bromley

23,000

20%

63,943

21%

Camden

77,000

24%

56,112

25%

City of London

93,000

22%

3,479

47%

Croydon

-19,000

-14%

74,513

20%

Ealing

16,000

11%

57,656

17%

Enfield

21,000

20%

75,066

24%

Greenwich

16,000

20%

59,286

23%

Hackney

34,000

31%

65,611

27%

Hammersmith and Fulham

42,000

30%

16,170

9%

Haringey

14,000

19%

58,199

23%

Harrow

16,000

22%

51,013

21%

Havering

14,000

18%

52,747

22%

Hillingdon

58,000

29%

77,815

28%

Hounslow

46,000

32%

70,099

27%

Islington

86,000

44%

60,154

29%

Kensington and Chelsea

32,000

24%

3,897

2%

Kingston upon Thames

7,000

9%

36,426

23%

Lambeth

48,000

33%

61,247

20%

Lewisham

16,000

22%

64,752

23%

Merton

29,000

35%

38,767

19%

Newham

45,000

52%

92,375

30%

Redbridge

22,000

30%

83,718

30%

Richmond upon Thames

14,000

15%

39,368

21%

Southwark

113,000

48%

63,678

22%

Sutton

5,000

7%

48,084

25%

Tower Hamlets

185,000

75%

103,223

40%

Waltham Forest

24,000

34%

66,065

25%

Wandsworth

31,000

26%

47,780

15%

Westminster

150,000

23%

59,216

27%

• To send feedback, e-mail amber.rolt@estatesgazette.com or tweet @amberrolt or @estatesgazette

With the DEI narrative shifting and companies and politicians stepping back from their previous commitments, it is more important than ever for those in the LGBTQIA+ community and their allies…