The volume and value of sales in the commercial auctions market are rising and there are “potential signs of a market turn” as yields show an underlying downward trend.

The latest Acuitus cPad report, which uses sales data from Essential Information Group, shows that Q2 sale volumes reached a record £206.3m – surpassing the previous Q2 peak of £202.3m in 2021 and 70% above the long-run average for the quarter.

This brought the total volume of H1 2024 sales of the assets Acuitus tracks to £423.3m, a significant increase on the previous H1 peak of £348m in 2021 and 58% above the long-run average.

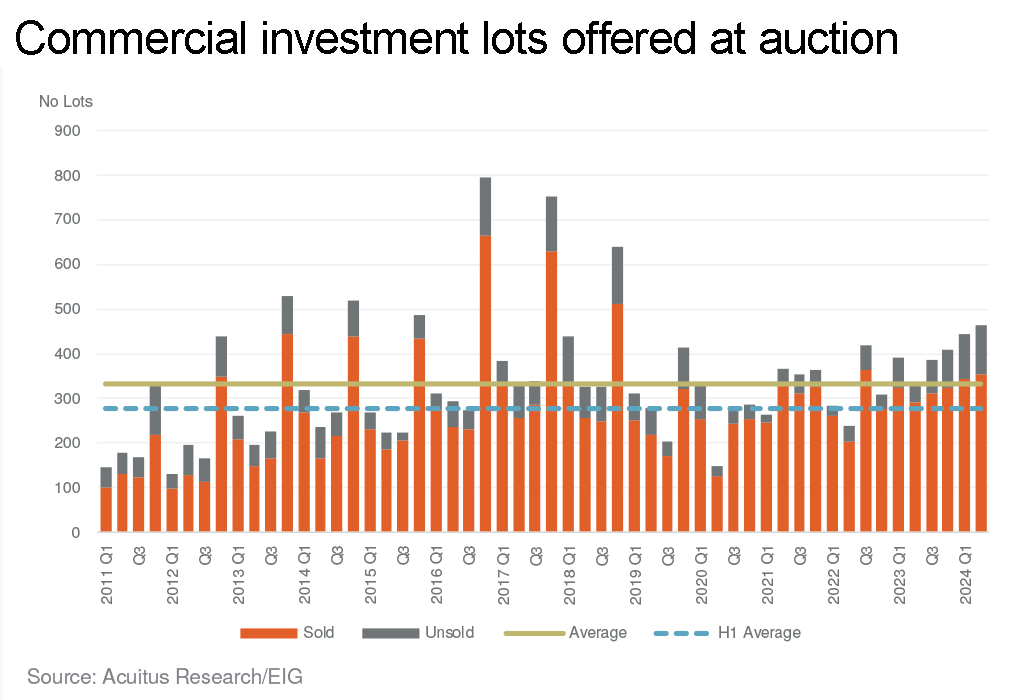

A total of 353 lots were sold in Q2 2024, compared to the previous peak of 329 lots in Q2 2021. The total number of lots sold in H1 was 696.

There has been a marked growth in the number of lots being offered for sale by auction. During the first six months of the year, 1,163 properties were listed – a 61% increase on the previous post-pandemic peak of 724 in 2021. However, this does include properties being listed in more than one subsequent auction. Discounting these, a record 907 were still offered at auction in HI 2024 – surpassing the previous peak of 764 lots in H1 2018.

On a less positive note, the overall sales rate fell to 76.1% – the lowest level since the shift to online auctions and pre-registration. The report suggests continuing political, economic and financial uncertainty played their part in this, keeping investors very price-sensitive.

Yields tighten

Retail and office yields are tightening. Retail yields are down by 160 basis points and office yields by 150 basis points. “While these improvements may be partly due to the quality of assets coming to market, the underlying trend in yields is downward,” the report says.

Looking at another measure, the weighted cPad All-Property average spot yield is down to 8.53% from the recent peak of 10.17% in Q1 2024. The report says this brings spot yields back to early 2023 levels, “indicating potential signs of a market turn although it’s still early days and investors are highly selective”. Spot yields are the actual yields for the current quarter and can be an early indicator of change.

Best value?

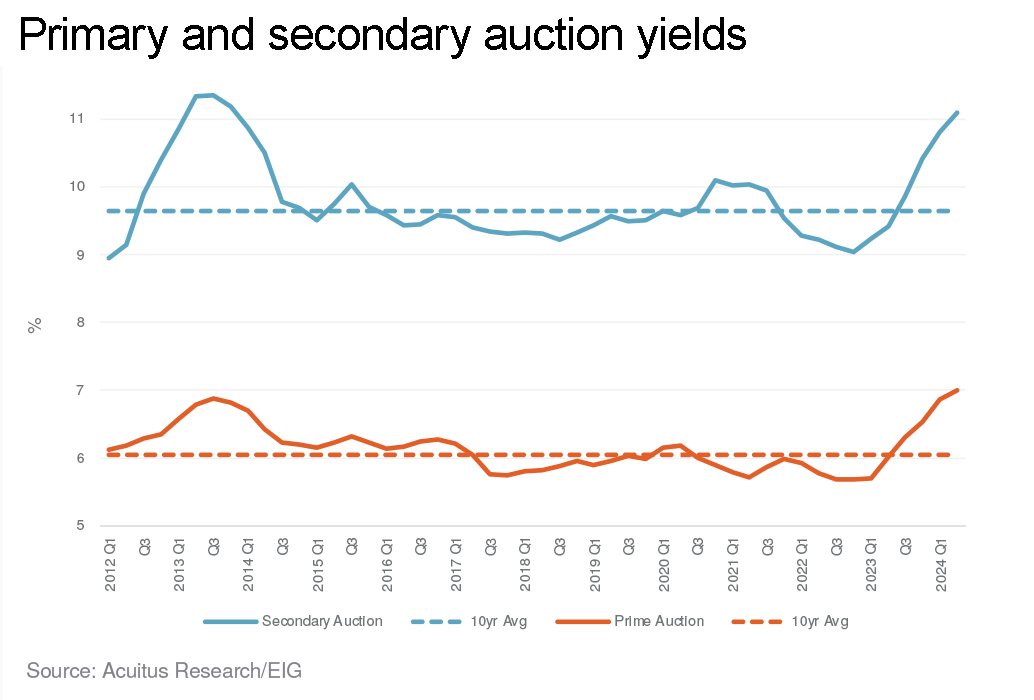

The report also calculates yields from the rolling averages of the spot yields for the previous four quarters. This smooths and prevents distortion from the impact from the varied compositions of different auctions. This shows that prime and secondary yields have not moved since the end of last year even though market sentiment has improved. As at the end of 2023, more than 400 basis points separate the two – twice the gap that prevailed 15 years ago.

The cPad All-Property Prime spot yield (lower quartile) remains at 7.04%, and the cPad All-Property Secondary (upper quartile) spot yield is at 11.25% with the yield gap sticking at over 400 basis points. The report says: “This continues to beg the question as to whether the current level of yields is beginning to offer some of the best value opportunities in more than a decade?”

London versus the rest of the UK

The cPad Average spot yield in London has sharpened by 80 basis points to 6.37%, but the most notable shift is across the Rest of the UK assets basket where the cPad Average spot yields fell by 160 basis points to 10.25%.

With investors still very focused on secure income, the cPad All-Property average spot yield on assets where the average lease terms are above five years has decreased by 75 basis points, while properties with shorter lease term profiles continue to move out.

Sector analysis

Alternatives: H1 2024 saw £107.1m of assets from outside the core sectors of retail, offices and industrial sold, with £54.1m of lots finding buyers in Q2. Typical lots in the alternatives category include properties which serve the medical, leisure and motor trade. Alternatives accounted for 25.3% of all lots sold by value in the year to the end of June. This was the highest six-month total since H2 2022, when £122m was transacted. Investors are increasingly drawn to assets with “sticky” occupiers who for reasons of licensing (medical), position (motor trade) or goodwill (leisure) are more likely to stay put and renew their leases.

London: A substantial segment of investors will look no further than the capital when finding their latest acquisition. In the second quarter of this year, £86.7m of London assets were sold to bring the H1 total to £167.3m – the highest on record, surpassing the previous high of £156.2m in H2 2022. The average lot size of London property sold in Q2 2024 was £1.17m, which was the second successive quarter when average sales prices were above £1m.

Retail: Retail assets remain the engine room of auction activity. During Q2, £129.8m of retail properties were sold, accounting for 62.9% of all sales. While this was below the long-run average of 67.6%, there is a clearly a reappraisal of retail investment currently taking place and Acuitus expects there to be increased investor interest as the year progresses and investors become more confident about the resilience and performance of certain assets. This shift in attitude is beginning to be evidenced by movements in retail spot yields.

Send feedback to Julia Cahill

Follow Estates Gazette