What will be the biggest disruptor for the industrial property sector over the next 12 months?

No part of the property market is evolving faster than logistics, which is now viewed as an integral component of the e-commerce revolution. What next? Can warehousing property continue to maintain such a breathtaking pace of change? The answer is unequivocally “yes”.

A Brexit-induced economic slowdown could have been the biggest near-term disruptor – but there has been no sign of that, quite the opposite. With our biggest, largely prelet, development pipeline and lowest portfolio vacancy rate ever, the demand drivers of e-commerce and convenience retail are transcending any economic uncertainties.

And so to the biggest disruptor of them all – Amazon. Now accounting for easily 10-20% of pan-European take-up, its new formats, including Fresh and Prime Now, make it avaricious for small urban as well as big box space. It will have become our third-largest customer inside 18 months – and is still growing. After shaking up general retail, it has now focused on food. And along the way it is reshaping logistics real estate. The use of robotics (making 20% cost savings) and automation combined with multi-level formats is challenging design status quo. With a fleet of aircraft reportedly on order, the question already stands: retailer or logistics provider? And, as a follow on, how much more disruption can it bring to the sector?

Much of Amazon’s success is through its use of technology. And it is in this arena that I think most disruption lies. Not in the next 12 months, more the next two decades. What is being tried now, though, will shape the future. Autonomous vehicle trials on the M6 could eventually challenge conventional hub-and-spoke location logic. More sci-fi, Amazon’s Prime Air and DHL’s Parcelcoptors are serious R&D investments, although yet to operate in anything but sparsely populated areas. Domino’s has delivered pizza by drone in Auckland, though. Maybe more believable is the Mercedes Vision Van – an electric van incorporating drones to deliver to doorstep.

It is breathless, intriguing and hard work, but being at the heart of changes to the way the world works and shops is exciting. Disruptive? For sure – but bring it on.

Andy Gulliford, chief operating officer, SEGRO

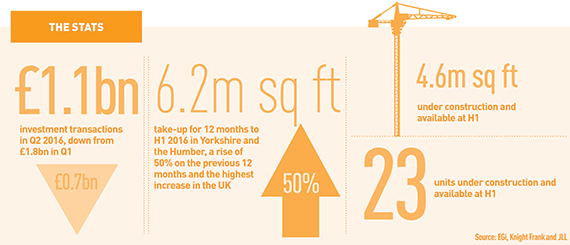

Demand may be steady but supply is short

When asked about business disruptors, many people will name innovators such as Uber and Airbnb, which are taking their markets forward in a completely different way. In industrial property, this is not the case. Rather than too much activity, the biggest disruptor in our sector over the next 12 months will be that there will not be enough.

To be specific, the hiatus that settled over industrial development before and after the EU referendum is changing the dynamics of our sector. While retail funds were monetising their investments as quickly as they could, the speculative development pipeline dried up. In the first half of 2016, around 9.5m sq ft of speculative buildings had been completed or were under construction. In the second half of the year, the amount of new space is likely to reduce dramatically.

But, customer demand is steady. Research carried out by Savills shows take-up in July and August this year – for both build-to-suit and speculative development – was 5m sq ft, the highest level for the period since 2008. At Prologis, we leased around 2.5m sq ft during these two months and we can see consistent demand continuing into 2017.

We are planning a new wave of speculative development in core logistics markets. But we can see that there will be a significant shortage of supply for the next 12 months. This means that pressure on build-to-suit development will increase and rents will rise.

Looking in more detail at new development, another disruptor will be increasing intensification of use, which is mainly due to the rapid rise of e-commerce. This has many implications, particularly the supply of power.

The UK power network is underfunded and already inadequate for some industrial and logistics operations. With the increasing use of electric vehicles and the continuing growth of e-commerce – our research indicates that it is likely to reach 6% of GDP by 2019 – the weakness of the network is likely to be a significant problem.

Andrew Griffiths, managing director, Prologis UK

In the news

Profits drop at Wolseley

Building supplies group Wolseley announced it was to close 80 branches and a distribution centre as its profits dropped 18%.

Hansteen goes on buying spree

Hansteen has bought the remaining £39.5m of shares in the Ashtenne Industrial Fund and has completed a £330m refinancing of the company. The fund owns 11.3m sq ft of multilet industrial properties in the UK, with a gross asset value of £436.4m.

Scottish rates changes spark demolition fears

Changes to rates relief in Scotland, which mean higher rates bills for empty industrial units, has led to fears that up to 3m sq ft of industrial space could be demolished to avoid the payment, predicts Colliers International. Starts on speculative development have also reduced as a result of the rates bill increase.

SEGRO seeks prelet funding

SEGRO is looking to raise £340m through a share placing to help fund prelet development projects across the UK.

Watch out for

Power up

Power up

The £18bn Hinkley Point C nuclear power plant has been given the green light, so expect development activity to start cranking up in the surrounding area.

Chunky deals

Private equity firms are beginning to exit the European logistics market, so look out for some big deals by institutional investors looking to boost their portfolios in the industrial sector.

Brexit

All eyes will be on H2 2016 figures to gauge just how much of an impact the EU referendum has had on the market. Agents predict reduced occupier demand and a cut in the number of speculative starts.

Expansion

As we go to press, a decision is imminent on London’s airport expansion. Wherever Theresa May bestows favour, it will have implications for cargo operations.