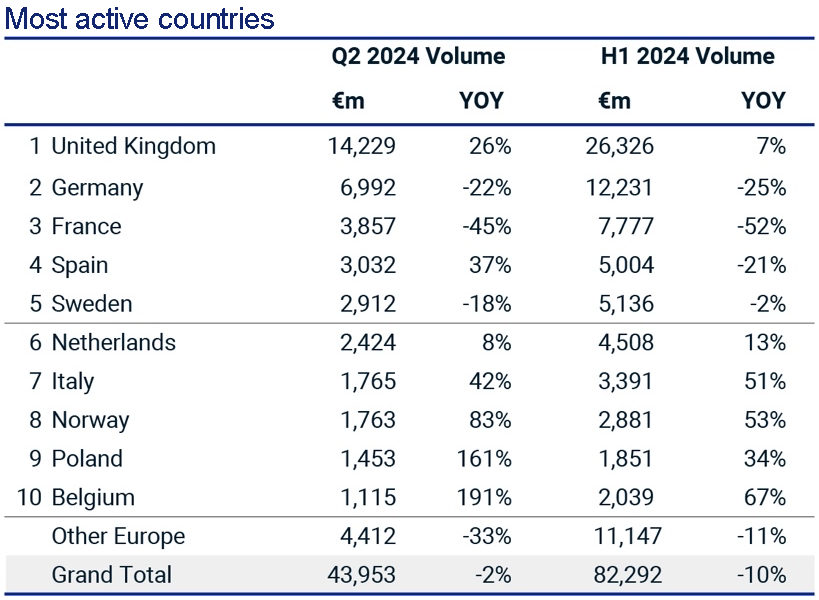

European commercial real estate investment levelled off in April through June 2024 after seven quarters of annual declines as a rebound in deal activity for the UK and some smaller markets offset the continued weakness of the German and French markets.

According to the latest Europe Capital Trends report from MSCI, the volume of completed transactions in the second quarter declined by 2% from a year earlier to €44bn (£37bn). This took property sales activity in the first six months to €82.3bn – down by 10% on the first half of 2023.

Tom Leahy, head of EMEA real estate research at MSCI, said: “It’s too soon to start celebrating, even if the worst of the downturn since mid-2022 may be behind us. The quarter’s data presents a very patchy picture for Europe’s investment markets that is likely to persist in the second half of the year.

“The office sector remains in the doldrums and in certain markets, notably France and Germany, there is still a gulf in price expectations between buyers and property owners looking to sell.”

He added: “The ingredients for a broader-based recovery are gradually coming together, nevertheless. Occupier demand has proved to be broadly resilient in most sectors throughout the downturn and pockets of the European market appear to have re-priced enough to start attracting investors. Prospects of lower interest rates will ease funding and pricing pressures, while there is capital ready for deployment at price points that allow transactions to happen.”

MSCI said the UK had been the first market where prices had undergone a substantial correction and was showing signs of being the first to rebound.

In Q2, transaction figures rose by 26% to €14.2bn in the UK, taking half-year volumes up by 7% on H1 2023.

London was the top-performing market, attracting €8.7bn of deals in H1, up by 4% on 2023.

UK offices, however, hit an all-time low, with just €2.7bn of deals done in the first half. Deals involving buildings in central business districts were down 71% on the 10-year average.

MSCI’s research confirms that from others, including EG Radius, that residential is now the most active sector for investment, overtaking the traditionally biggest market of offices.

Investor demand for hotels has also rebounded post-Covid, said MSCI, in line with the recovery in international travel and tourism as well as the ongoing shift towards assets requiring operational expertise.

Image by Pete Linforth/Pixabay

Send feedback to Samantha McClary

Follow Estates Gazette