If there was a time to be an investment agent in Dublin, it was almost certainly last year.

If there was a time to be an investment agent in Dublin, it was almost certainly last year.

Direct property investment into the Irish Republic reached a staggering €4.6bn (£3.4bn) in 2014, way more than double the previous year’s total, and significantly up on the €3.2bn recorded at the last high point in 2006.

Before investment agents from the UK and elsewhere cut a dash to the Emerald Isle to make their fortunes, they should know that last year’s performance was a one-off, driven by National Asset Management Agency disposals (see below) and large sales at the International Financial Services Centre.

Not that the prospects for 2015 are anything to complain about. In fact, they are rather good, thanks to a buoyant Irish economy and a healthy supply of product.

Consensus forecasts suggest that Ireland’s GDP growth this year will be greater than 4% – a big step ahead of the EU average of 1.5%. This is an impressive turnaround for an economy that was subject to an EU bailout as recently as 2013.

This favourable climate, combined with record low interest rates and a relatively weak euro, make Ireland an attractive target for foreign investors.

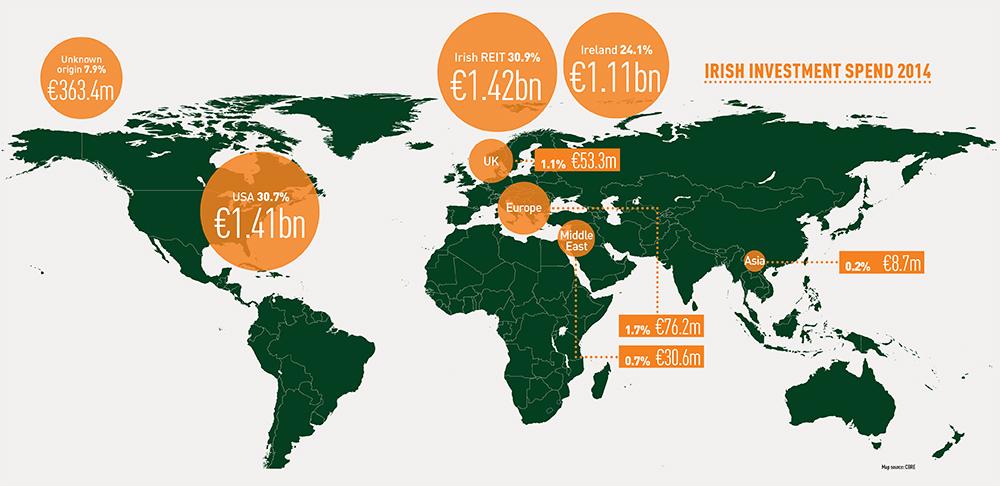

Last year, US investors stormed into a market that, until recently, was dominated by domestic buyers. The Americans, according to CBRE, accounted for nearly one-third of 2014’s total investment spend – that is €1.4bn (see map).

They will face greater competition this year, says CBRE Ireland executive director and head of research Marie Hunt: “German investors are likely to be active. And up until now Asian money has not really looked at Ireland because the lot sizes were too small. Now that Nama has increased portfolio sizes (see box, p93), they may be more interested.”

One of last year’s surprises was the €500m invested in multi-family properties. “Residential simply wasn’t an asset class here before,” says Adrian Truieck, Irish investment property director at Knight Frank. Multi-family deals this year may be limited by lack of stock but, as an alternative, student housing is on the horizon (see below).

In the meantime, Nama disposals will probably be the biggest show in town. “There’s a very clear supply pipeline, so we are likely to see yield compression for at least the next 12-18 months,” says Johnny Horgan, CBRE Ireland’s head of capital markets.

A large amount of space still in Nama’s pot is the 40 acres in Dublin’s Docklands, designated as a strategic development zone. Just before Christmas, Nama brokered a deal (previously codenamed Project Wave) with joint venture partners Oxley Holdings and Ballymore to develop 5.8 acres at 72-80 North Wall Quay as mixed-use. It will include 200 apartments and 645,000 sq ft of offices. The amount the jv partners will pay Nama for the long leasehold is yet to be disclosed, but Nama will retain the freehold, as well as taking a cut from future development sales.

Will a similar deal be done in Docklands in 2015? A Nama spokesperson says: “Nama is not wedded to any particular approach when setting strategy for individual Docklands SDZ sites. For each site, it will be a matter of which strategy offers the best risk-adjusted return for Nama. We also see the Docklands SDZ being developed on a phased basis, with new construction being funded in line with proven prospective demand, rather than on a purely speculative basis.”

While the bank can provide up to €1.9bn in development funding, it has made it clear that, in the current climate, it expects investors to pick up a substantial part of the funding tab. With last year’s record level of capital rolling into town, there is likely to be no shortage of takers.

Nama disposals

Until relatively recently, Irish bad bank Nama was expected to dispose of its portfolio in dribs and drabs over an extended period of time.

That changed last year when, only five years after the organisation was set up, it saw unprecedented purchaser interest. Last summer, the bank announced that it would accelerate disposals, aiming to redeem all senior debt by 2018.

The market response to larger lot sizes was conclusive: the €4.5bn Project Eagle portfolio (containing all Northern Ireland holdings), snapped up by Cerberus Capital, was the largest single transaction to date.

Continued investor interest in 2015 has led to speculation that the programme could be speeded up further. A Nama spokesperson insists that there has been no strategy change, but concedes that packages brought to market may well exceed the €250m quarterly minimum announced in October 2014.

Last month, Nama put its mammoth Project Arrow up for grabs, an €8.4bn portfolio of non-performing loans secured on mixed-use properties in Ireland and the UK. Cerberus is frontrunner to win what is likely to be a complex trophy, but it may have to beat off some competition, not least from other American firms.

“US investors see Ireland as a country protected from other parts of Europe (for example, Greece), so we are likely to see strong interest from them this year,” says Federico Montero, head of EMEA loan sales at Cushman & Wakefield, which is advising Nama on the Project Arrow sale. He adds that more German money is likely to be searching for Irish opportunities, along with the US debt purchasers.

New opportunities in Student housing

One of the UK’s most up-and-coming alternative investment sectors – student housing – may not yet be up in Dublin, but it is most certainly on its way. After several years of virtually no development activity in the sector, the past 12 months have seen a flurry of proposals head towards Dublin’s planners.

UK developers such as Knightsbridge, which is planning a €40m, 500-bed block in the Liberties area, and Mortar Developments, which is aiming to build a €30m, 232-bed scheme on Church Street, will be among the first to create a new generation of bespoke student accommodation.

Dublin is attractive to UK specialist housing providers that have grown confident in securing demand for their product and are now finding that opportunities are harder to come by. An Irish government drive to boost Dublin’s students by half (swelling the ranks of the city’s existing 82,000 full-time scholars by an additional 41,000) has certainly helped, but the existing supply differential is already tempting – existing private purpose-built housing can cater for only 3% of Dublin’s student body.

Up to 5,000 beds could be delivered within the next three years; Mortar alone expects to build 1,000 of them. But development may yet be stymied by construction cost inflation, non-recoverable VAT on construction costs, competing land uses and the relatively low level of private sector rentals (around €200 per week).

Assuming several projects come forward as planned, the first investment sales could be seen early next year. “Dublin will be seen by investors as an offshoot of the UK model, where there is now a quantum of stabilised stock,” says Sam Ball, senior surveyor in Knight Frank’s student housing team.

Until transactions occur, pricing will be based on sentiment. “We believe that prices will be 50 basis points ahead of regional UK returns.” However, investors are unlikely to step outside Dublin, as development returns do not yet stack up in other Irish centres such as Cork, Limerick and Galway.