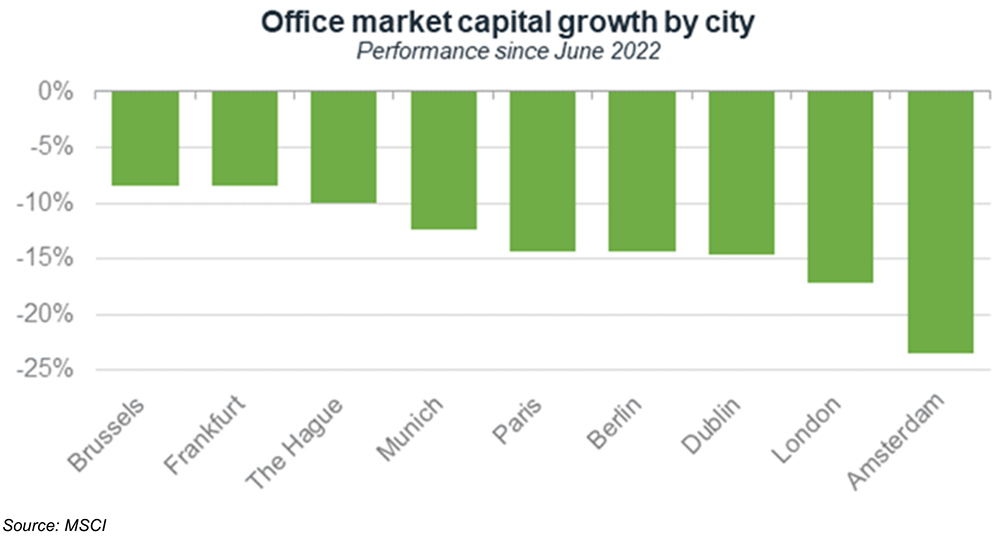

London’s capital values are correcting faster than all but one of its European rivals.

New data analysed by BNP Paribas Real Estate showed capital growth for London’s office sector declining by 17.1% year-on-year.

Further analysis of the data for office market capital growth over the same period across eight additional key markets – Amsterdam, Berlin, Dublin, Hamburg, Frankfurt, Milan, Paris and The Hague – revealed the office sector in the UK capital had corrected the most since June 2022, with the exception of Amsterdam.

The firm said the figures suggested that London was in the final stages of absorbing the price correction which started in Q2 2022.

Fergus Keane, head of central London investment markets at BNP PRE, said: “The London office sector is offering a very rare entry point for investors for either repriced core product, or those with the means to spend capex to reposition assets into the core market.”

London office capital growth has underperformed most European gateway markets since 2019.

Office investment volume have remained subdued, with £1.3bn transacting during Q2, equating to a fall of 49% year-on-year. Turnover for H1 2023 was £4.77bn, a downturn of 40% year-on-year.

Keane added: “For a decade, it has been a seller’s market, and that has now flipped, with buyers holding the upper hand, particularly if you are an all-equity player.”

A cheap pound is already attracting overseas investors. European investment into central London offices accounted for more than 21% of total volumes in Q2, an increase of 18% in comparison to H1 2022. Some 42% of all central London office investment during the first half of the year was from Asia Pacific-based purchasers.

However, Keane cautioned: “This entry point won’t last long.”

Analysis of previous downturns shows yields can come in quickly when interest rates start to fall, and this is expected to come through in the first half of 2024.

“I expect this window of opportunity will be closing this time next year.”

Keane said there were fundamental differences between the market now and in 2008.

“It actually shares more characteristics with 2011/12 on the real estate cycle clock,” he said.

While debt has become more expensive, it still remains available. “And there is a lot more dry powder waiting to be deployed today,” Keane said.

There is also much less distress in the market, with fire-sales rare and assets coming to the market selectively.

In addition, the market is coming off a 10-year cycle of low supply, while occupier demand for grade-A buildings remains high, driving rental growth.

“These are compelling indicators for what’s about to come,” said Keane. “Equity investors need to be serious to secure opportunities, examining opportunities now and early into the new year in order to be ready to take advantage of other buyers being forced to wait on the sidelines due to the high cost of finance. Market sentiment suggests yields could drift a little further by year end, which I expect might represent the peak.”

To send feedback, e-mail piers.wehner@eg.co.uk or tweet @PiersWehner or @EGPropertyNews