London will have the highest amount of surplus space of all of Europe’s major office markets by 2033.

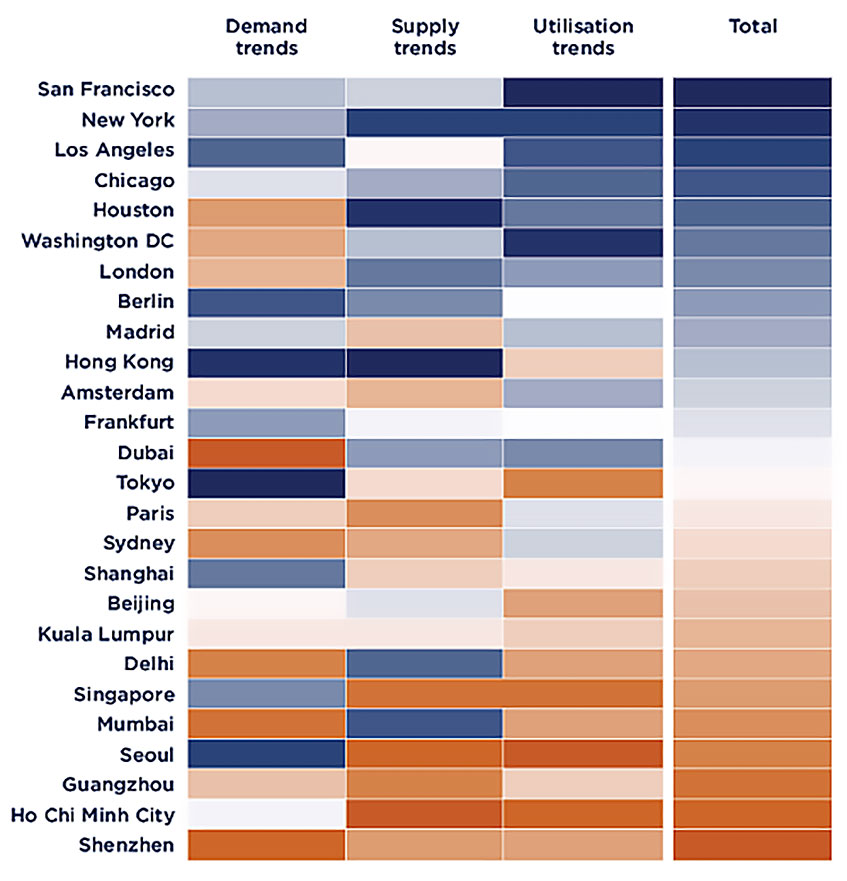

An analysis of 26 global cities by Savills has revealed a “broad East-West divide”, with Chinese cities, Singapore and Seoul predicted to have the lowest excess supply and cities in the USA expected to have the greatest availability.

European cities are expected to sit largely in the middle of the pack, with supply/demand dynamics remaining roughly in balance. But London is right on the edge of that block, showing an inclination to oversupply.

Kelcie Sellers, associate at Savills World Research, said: “This isn’t about offices just becoming empty due to some cities seeing lower return-to-work levels post-pandemic. It’s about how long-term economic, demographic and development trends interact with working patterns, to determine which cities potentially need to focus most closely on retrofitting and repurposing excess office space to other uses.

“Our analysis shows a broad East-West divide as office use in Asia-Pacific is supported by expanding service economies, younger populations, cultural factors, a limited supply of buildings and newer ‘greener’ stock. Elsewhere, the future supply dynamic is more nuanced, due to projected lower utilisation rates and an oversupply of pre-2010 buildings, which tend to have lower sustainability credentials.”

Savills said it had looked “beyond the headlines about workers returning to the office and current utilisation levels”, to establish how current trends would interact with projected economic growth, demographics, development pipelines and volumes of “green” office stock.

This allowed the team to generate a picture of what office availability in key markets around the world is likely to look like a decade from now.

In the US cities with the highest projected availability over the longer term, Savills noted that many occupiers have begun implementing return-to-office mandates this year, which could help office demand increase in the short term and will chip away at the oversupply of space in some locations.

Jeremy Bates, Savills’ EMEA head of occupational markets, added: “While there have been many headlines about corporate occupiers’ space strategies, largely led by some turbulence in parts of the tech sector, the fact is that quality office space remains in high demand.

”Long-term, however, we need to consider all the factors that generate tenant demand, and accept that in some locations this will lead to the office market looking quite different in 10 years’ time, with occupier requirements centring around an increasingly narrow definition of ‘prime’ space.”

But Savills is not predicting a dystopian future of hollow city centres or economic collapse for those cities with predicted oversupply.

Eri Mitsostergiou, a Savills World Research director, said: “Where higher office availability levels are present, there are opportunities for repurposing: in central locations, there is often both the demand and the potential for residential property conversions, or for last-mile logistics space in more suburban locations. Regardless of the end use of the repurposed office, cities becoming more mixed-use across the world will provide opportunities for repositioning and revitalisation.”

Future Office Availability Index

Note: The index is colour-ranked from markets most likely to see an increase in office availability (dark blue) to those least likely (burnt orange). Each category is individually colour-scaled. Utilisation trends is given a half weighting. Demand trends and supply trends are equally weighted.

Source: Savills Research, using data from Oxford Economics, Kastle Systems and local sources

To send feedback, e-mail piers.wehner@eg.co.uk or tweet @PiersWehner or @EGPropertyNews

See which agents are doing the most deals in the London submarkets with our On-Demand Rankings >>