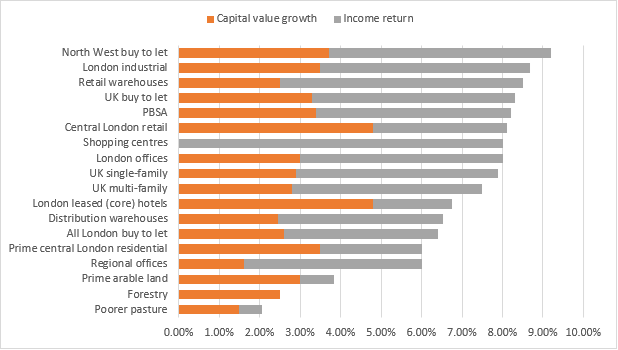

Residential buy-to-let in the North West, London industrial property and retail warehouses are set to be the UK property market’s top performers from this year, according to Savills.

The agent predicts these three sub-sectors will experience annualised investment returns of between 8.5% and 9.2% between 2024 and 2028.

A further five asset classes are expected to see returns in excess of 8%: UK buy-to-let; purpose-built student accommodation; central London retail; shopping centres; and London offices.

Savills annual cross-sector forecast suggests a stronger outlook and opportunity for UK property investment in 2024 as interest rates steady. But returns will continue to be driven by income potential instead of capital growth.

Commercial

Opportunistic investors will be attracted to parts of the retail market by rebased rents and rates, and higher yields, as well as the medium-term capital growth upside that could come from change of use, said Savills. Occupier demand for prime high-quality and highly rated warehouses, meanwhile, is also set to keep prices rising in 2024, especially in London.

After an uneven year for the UK office market, cooling inflation, falling borrowing costs and good rental growth prospects will bring some development schemes back into viable territory in 2024, as investors look to capitalise on the undersupply of prime and green office space.

Residential

Turbulence in the mortgage markets, an uncertain planning environment, increased build cost inflation and regulatory changes in the private rented sector all served to suppress transactions and growth in the residential sector in 2023. But with inflation heading back towards the Bank of England target of 2% and more stability in the mortgage markets, Savills expects to see the primary sources of financial disturbance ease back over the course of next year.

Conditions remain tough for landlords, but with Savills forecasting rents to grow by a further 18.1% by 2028 there is still significant opportunity for those less reliant on debt. Those with a portfolio furthest from London look best placed, with Savills forecasting 9.2% returns for the North West.

But struggles in the private rented sector are also expected to spur on institutional landlords, and both build-to-rent and PBSA are expected to play an increasingly important role looking forward.

Rural

UK farmland is viewed as the asset class most likely to help the government meet its environmental targets. It continues to provide long-term capital growth and, in 2023, global conflicts reinforced the importance of UK land producing food, fuel and fibre.

Prime arable land focusing on food production will continue to be in demand, especially that with access to a reliable water supply. Savills has forecast capital growth of 3% for prime arable land.

The UK forestry market slowed over 2023 from its peak in 2021. However, the investment opportunity that land offers as the UK continues to work towards net zero emissions by 2050 (2045 for Scotland) is still significant. Savills forecasts that grade 3 arable land could provide the optimum balance of risk owing to its flexibility. It will appeal to agricultural buyers as well as those motivated by nature-based solutions and natural capital.

Richard Merryweather, Savills joint head of UK investment, said: “The factors that drove falls in UK property values and transaction levels over the last two years are expected to improve in 2024. There will be significant opportunity – especially in the commercial and residential spaces – for investors to buy at the bottom of the market, with a focus on opportunities where capital values have either over-corrected, or where rental growth prospects might be accelerating.

“The UK is one of 40 countries that is expected to have an election in 2024, which often causes investor uncertainty. However, our analysis suggests that although transactional activity is generally lower than normal in the three months prior to the election date, it recovers over the following six months.

“The rationale for investing in land and property remains good, particularly for investors who are looking for infrastructure-type investments that deliver comparatively predictable income streams over the long term. A rising interest in food security and carbon reduction is likely to boost investor interest in these segments. We are seldom able to see the bottom of any cycle this clearly, but we are confident that 2024 and 2025 will be the years in which normal service will be resumed.”

To send feedback, e-mail julia.cahill@eg.co.uk or tweet @EGJuliaC or @EGPropertyNews