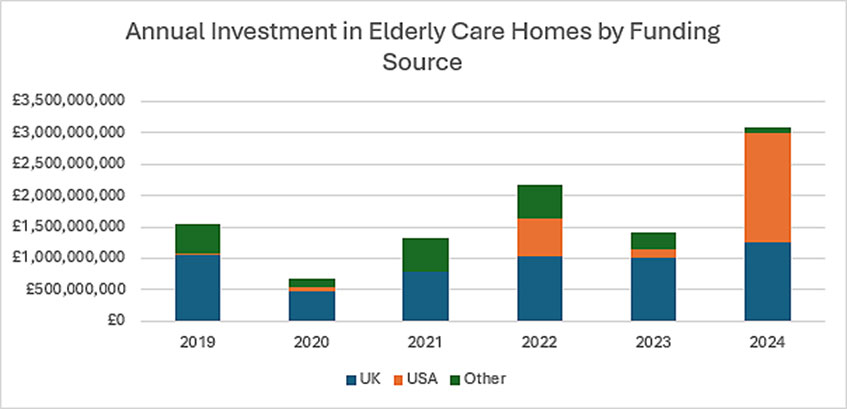

The UK’s elderly care home market saw a record £3.1bn of deals in 2024, driven by a surge in activity during the second half that amounted to £2.3bn.

According to data from Cushman & Wakefield, the final quarter of the year was the most active since tracking began in 2019, with a total of £1.3bn of transactions.

The agency said that several factors sit behind the growth in deal volume, the standout being an influx of capital from US-based investors, which surged from 10% of overall volume in 2023 to more than 56% in 2024.

This was influenced by US real estate investment trust Welltower’s whole company acquisition from Bridgepoint of Care UK, which operates 163 care homes, making it one of the UK’s largest chains. In addition, Omega Healthcare Investors, PGIM and others were also highly active and continued to show strong appetite for UK assets.

Specialist investors from across the globe reaffirmed their dominance in 2024, with a large proportion of the US investment falling into this group, accounting for nearly £2.2bn of total volume.

Analysis shows that the past 12 months also saw a shift in the placement of money. Previously, low interest rates and a buoyant investment market had PropCo structures driving deals, allowing investors to limit exposure to operational risk while tenants take income streams at zero or modest entry costs.

In contrast, 2024 saw OpCo and WholeCo transactions at the forefront at 72% of all volume, helped in part by some specialist investors willing and able to acquire operational income streams through RIDEA structures while their UK and European equivalents focus on rental income streams only.

Overall, the UK remains a key market for specialist healthcare investors, with the combination of stable returns, demand-driven growth and the ability to achieve economies of scale underpinning investment strategies.

Tom Robinson, head of healthcare at Cushman & Wakefield, said: “The past 12 months have seen interest and activity surge in the UK, driven by strong market fundamentals. Some of this activity was underpinned by eye-catching trophy deals from US investors, but we also saw the same parties deploying capital in smaller tranches, showing the overall trend to be more than a one-hit wonder.

“Major transactions of scale are less commonplace in a diversified space such as the care market, and some suggest that the absence of these may hamper overall activity levels in 2025, but the pipeline of potential deal flow still looks robust and interest remains high. The influx of US capital is somewhat based on opportunism and the inability of UK REITs and European investors to raise money. This has allowed US investors to increase market share.

“Specialist investors naturally remain a strong part of the market, but the UK’s overall attractiveness means that we can expect non-specialist capital to be targeting the sector as well. We expect that many funds will be seeking capital to utilise in the UK healthcare market, with a particular focus on the PropCo segment.”

Photo © Shutterstock

Send feedback to Akanksha Soni

Follow Estates Gazette